- Yes, you can legally be fired after announcing your retirement due to at-will employment laws. However, if your employer fires you specifically to steal your unvested pension (an ERISA violation) or replaces you due to age bias (an ADEA violation), it is illegal wrongful termination.

You have worked hard for decades, and you are finally ready to step away. But a terrifying question keeps you up at night: can I be fired after announcing my retirement? You might want to do the “right thing” and give your boss six months to find a replacement. Unfortunately, in corporate America, professional courtesy can financially ruin you.

In 49 out of 50 states, giving a long retirement notice strips you of your leverage. This 2026 survival guide flips the traditional script. We will teach you how to treat your retirement announcement as a ruthless financial transaction. You will learn how to protect your pension, qualify for hidden severance packages, and force your employer to pay unemployment if they try to push you out early.

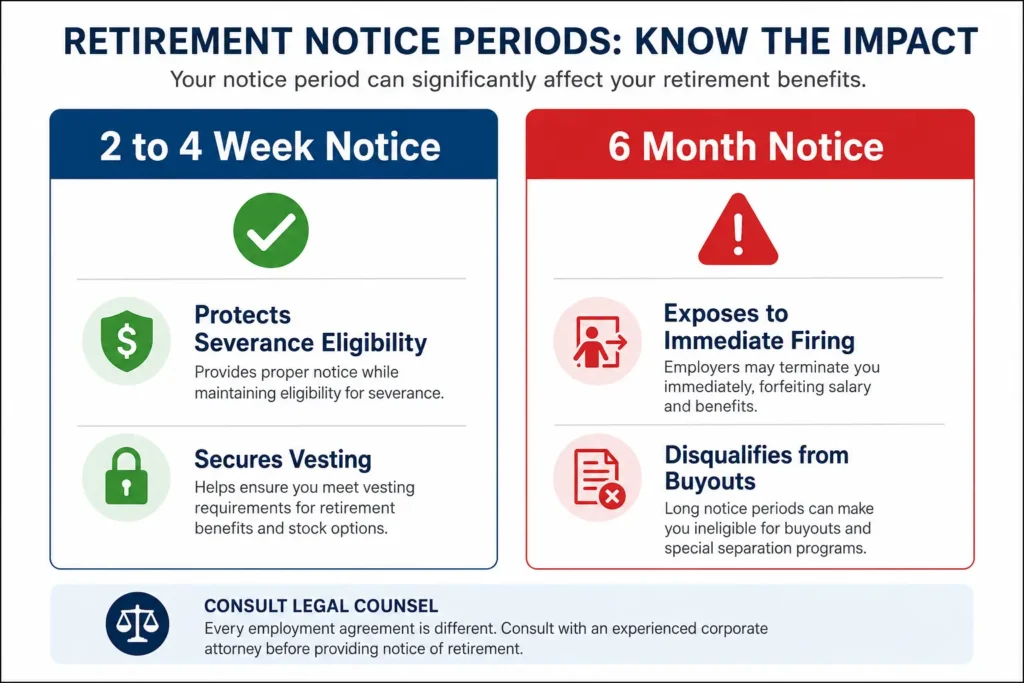

Why is giving a 6-month retirement notice a dangerous trap?

Giving a long retirement notice exposes you to immediate termination under at-will employment. It also legally disqualifies you from lucrative Voluntary Separation Programs (VSPs) or corporate severance packages, as employers will not pay severance to an employee who has already announced their departure.

The biggest mistake older workers make is treating their employer like family. You might think giving a six-month notice is polite. To Human Resources, it is an opportunity to save money.

Because of at-will employment, your boss can accept your six-month notice and fire you that exact same afternoon. They do not have to pay you for those remaining six months.

Worse, announcing early destroys your chances of catching a Voluntary Separation Program (VSP). In 2026, companies frequently downsize by offering massive severance packages (often 6 to 12 months of pay) to older workers who volunteer to leave. If your retirement letter is already on file, HR will exclude you from the buyout. Why would they pay you $50,000 to leave when you already told them you are quitting for free?

What is the ERISA vesting cliff and how does it protect me?

The Employee Retirement Income Security Act (ERISA) makes it a federal crime for an employer to fire you to prevent your pension or 401(k) match from vesting. If you are fired right before a vesting cliff, you have grounds for a massive federal lawsuit.

If your employer fires you right after you announce your retirement, look at the calendar. Are you close to a financial milestone?

Many companies use a vesting cliff for their 401(k) matches or pension plans. For example, you might only get to keep the company’s 401(k) contributions if you hit exactly five years of service. If you give notice at four years and eleven months, and they fire you the next day, they steal your unvested money.

This is highly illegal. The Employee Benefits Security Administration (EBSA) strictly enforces the Employee Retirement Income Security Act (ERISA). If you can prove your employer fired you specifically to prevent your retirement benefits from vesting, you can sue them in federal court for every penny they tried to keep.

Can I collect unemployment if I am fired before my retirement date?

Yes. If you give a 60-day retirement notice and your employer fires you on day two, they have involuntarily severed the relationship. You are legally entitled to collect Unemployment Insurance benefits for the remaining 58 days of your notice period.

Many workers assume that because they planned to quit, they cannot get unemployment. This is a myth.

Unemployment Insurance is based on who officially severs the employment tie. If you hand in a formal letter stating, “I intend to retire on December 1st,” you are offering to work until December 1st.

If your boss says, “Actually, today is your last day,” the boss just fired you. Because they ended the employment prematurely, you can immediately file for unemployment benefits. You will collect weekly checks to bridge the financial gap between your unexpected firing and your actual retirement date.

What is constructive discharge for older workers?

If your employer does not fire you but intentionally creates a hostile work environment to force you to quit early, this is called a constructive discharge. Quitting under these conditions allows you to sue for age discrimination and collect unemployment benefits.

Sometimes an employer does not want to fire you because they fear an Age Discrimination in Employment Act (ADEA) lawsuit. Instead, they try to make you miserable so you leave on your own.

They might suddenly demote you, slash your hours, or transfer you to a terrible shift. They want you to quit early so they do not have to pay out your accrued vacation time or end-of-year bonuses.

In employment law, this is called a constructive discharge. The law treats this exactly the same as being fired. If you document the sudden abuse and quit, you can file a claim with the Equal Employment Opportunity Commission (EEOC) for age discrimination.

Practical Case Study: Losing Severance by Announcing Too Early

A senior manager gave a one-year retirement notice out of professional courtesy. Six months later, the company announced a massive corporate restructuring. Because his retirement was already on file, HR legally excluded him from a $60,000 severance package offered to his laid-off peers.

Understanding the financial risks of an early notice is crucial. Let’s look at a real-world disaster scenario.

The Situation: “Robert,” a 63-year-old regional director, decided he wanted to retire at 64. Out of loyalty to his team, he gave his VP a written one-year notice to help train his replacement.

The Action: Seven months into his notice period, the corporation merged with a competitor. They initiated a massive Reduction in Force (RIF). They offered all regional directors a voluntary buyout package: one year of full salary and fully paid COBRA health insurance if they agreed to leave.

The Result: Robert eagerly applied for the buyout. HR denied his application. The legal terms of the Severance Package explicitly excluded any employee who had already submitted a notice of resignation or retirement. Robert was forced to work his final five months and left with absolutely nothing, missing out on a $120,000 windfall purely because he was trying to be “polite.”

Frequently Asked Questions (FAQ) About Retirement and Job Security

What happens to my 401(k) if I am fired before my retirement date?

Your personal contributions to your 401(k) are 100% yours and cannot be taken away under any circumstances. However, if your employer matches your contributions, you must check your vesting schedule. If you are fired before those matching funds vest, you lose the employer’s portion entirely.

How do I write a protective retirement letter?

Keep it brief and factual. Do not write a three-page emotional essay. State clearly: “Please accept this letter as formal notification that I am retiring from my position, effective [Exact Date].” Do not write “I am resigning immediately” if you intend to work for two more weeks. Keeping the date clear protects your right to claim unemployment if they force you out early.

What happens to my health insurance if I am fired before Medicare kicks in?

If you are fired before you turn 65, you will lose your employer-sponsored health insurance. However, you are legally entitled to continue your exact same coverage through COBRA for up to 18 months. You will have to pay the full premium yourself, which is expensive, but it guarantees you will not experience a gap in medical coverage before Medicare begins.