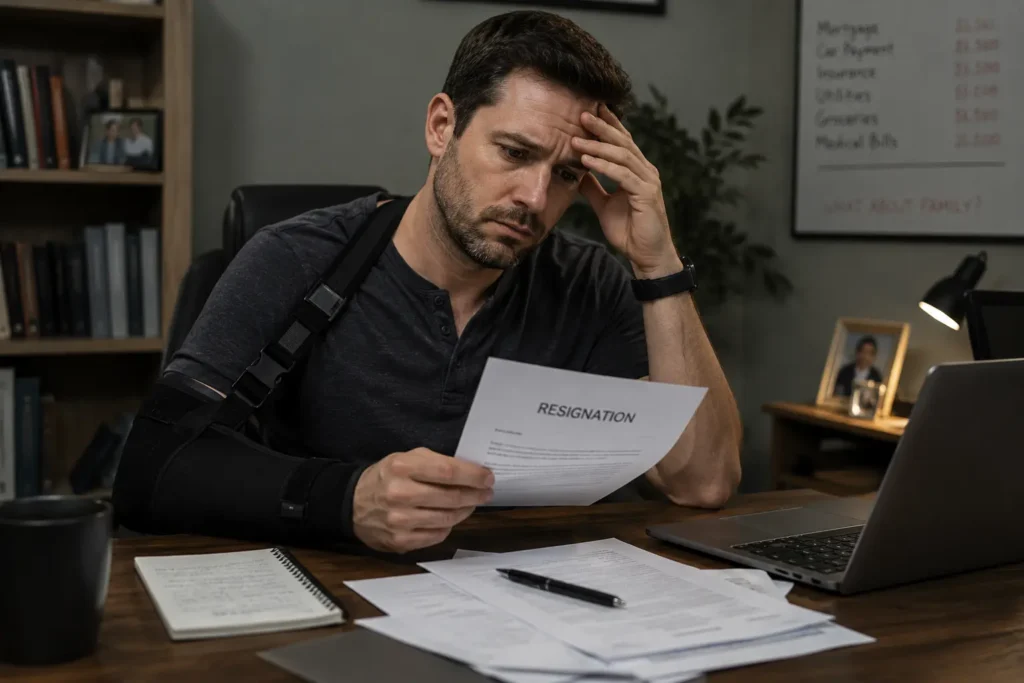

If you are dealing with a severe workplace injury, a hostile boss, or an uncooperative HR department, you might be at your breaking point, wondering: can I quit my job while on workers comp? It is completely understandable to want to walk away from a toxic environment, but resigning at the wrong time can financially devastate your recovery.

- Yes, because of at-will employment, you can legally quit your job while on workers’ comp. However, voluntarily resigning usually destroys your right to receive ongoing wage replacement checks. You should never quit without negotiating a lump-sum settlement or consulting an employment lawyer first.

This 2026 legal guide is your survival manual. We will explain exactly how quitting impacts your weekly checks, why insurance companies want you to resign, how the “light-duty” trap works, and the exact steps you need to take to protect your money and your medical care.

Do I lose my workers’ comp benefits if I quit my job?

If you voluntarily quit your job, you will almost certainly lose your weekly Temporary Total Disability (TTD) or wage replacement benefits. The insurance company will legally argue that your loss of income is due to your resignation, not your workplace injury.

Workers’ compensation is divided into two main parts: medical benefits and wage replacement.

If your doctor says you cannot work while you recover, the insurance company pays you a percentage of your lost wages (usually two-thirds). However, if you say, “I quit,” the legal narrative shifts. The insurance adjuster will immediately file a motion to stop your checks. They will argue to the judge that they no longer owe you money because you chose to stop working.

By quitting, you hand the insurance company a massive legal victory. They no longer have to pay your weekly wages, which severely weakens your leverage to negotiate a fair final settlement.

What happens to my medical bills after I resign?

Your workers’ compensation medical benefits generally continue even after you resign. The insurance company remains legally responsible for paying for your injury-related surgeries, physical therapy, and medications until you reach Maximum Medical Improvement (MMI).

This is the one silver lining. Your right to medical care is tied to the date of the injury, not your employment status. If you quit, get fired, or the company goes bankrupt, the workers’ compensation insurance carrier must still pay the doctors treating your specific work injury.

However, be warned about your general health insurance. If you quit, you will likely lose your employer-sponsored health insurance (though you can pay for COBRA). Workers’ comp only covers the specific body part you injured. If you quit and lose your primary health insurance, you will have no coverage for routine illnesses or unrelated medical issues.

The “Light Duty” Trap: Can I quit if the modified work is unfair?

Employers often offer frustrating “light-duty” jobs to avoid paying wage benefits. If you quit because you hate the modified work, you forfeit your benefits. You can only refuse light duty if your doctor officially states the job exceeds your physical medical restrictions.

In 2026, the “Light-Duty Trap” is the most common tactic employers use to force injured workers to quit.

Let’s say you hurt your back in a warehouse. Your doctor clears you for “light-duty, desk work only.” To avoid paying your wage replacement benefits, your boss offers you a light-duty job staring at a security monitor in a cold, isolated room for 8 hours a day.

They want you to get bored and frustrated. They want you to quit.

If you quit because the job is demeaning or boring, you lose your workers’ comp checks. The only legal way to reject a light-duty assignment is if the physical demands of the job violate the exact written restrictions provided by your treating physician.

Should I negotiate a lump-sum settlement before quitting?

Yes. You should never resign before leveraging your employment status into a lump-sum settlement. An experienced workers’ comp attorney can negotiate a payout that covers your future medical needs and lost wages in exchange for your voluntary resignation.

If you hate your job and want to leave, do not just hand in your two weeks’ notice for free. Your employment status is your greatest negotiating chip.

Insurance companies want to close cases. If you are still an employee, they face the risk of you returning to work, getting re-injured, and costing them more money.

If you have reached Maximum Medical Improvement (MMI)—meaning you have healed as much as you ever will—your lawyer can approach the insurer. They can negotiate a final lump-sum settlement (often called a Clincher or Section 32 agreement). You agree to close the claim forever, and in return, they hand you a large tax-free check.

Can my employer force me to sign a resignation agreement?

It is highly common for insurance companies to require you to sign a voluntary resignation agreement as a mandatory condition of a lump-sum settlement. However, an employer cannot legally force or threaten you to resign before a settlement is reached.

When you finally agree to a lump-sum payout, the paperwork will almost always include a “Voluntary Resignation and Release” clause. The employer is basically saying: “We will pay you this large settlement, but you must legally resign and promise never to apply for a job here again.”

This is completely legal and standard practice in 2026. However, if your boss pulls you into an office before a settlement is negotiated and threatens to fire you unless you quit, that is illegal retaliation.

Practical Case Study: Quitting Due to a Hostile Work Environment

If your employer makes your workplace intolerable after an injury, forcing you to resign, it is considered a “constructive discharge.” A recent case saw a worker win massive damages after proving their boss harassed them daily for filing a workers’ comp claim.

Sometimes, you truly have no choice but to quit because your boss is making your life a living hell. In employment law, this is called a constructive discharge.

The Situation: “Sarah” tore her rotator cuff and filed a workers’ comp claim. Her doctor cleared her for light duty. However, when she returned, her manager was furious that her injury increased the company’s insurance premiums. The manager began insulting her daily, denying her legally mandated breaks, and assigning her light-duty tasks in a physically isolated, unheated supply closet.

The Action: Sarah documented every insult, took photos of the closet, and sent an email to HR complaining of retaliation. HR did nothing. The stress caused Sarah to suffer panic attacks, and she finally quit to protect her mental health.

The Result: Sarah hired an employment lawyer. Because she quit due to illegal harassment directly related to her injury, she did not just keep her workers’ comp benefits—she filed a separate lawsuit for retaliation and wrongful termination. The employer was forced to settle for a massive six-figure sum to avoid a public jury trial.

Frequently Asked Questions (FAQ) About Quitting on Workers’ Comp

Can I get a new job while on workers’ comp?

Yes, but you must be incredibly careful. If you accept a new job while receiving Temporary Total Disability (TTD) checks, you are committing insurance fraud. You must immediately notify the insurance company of your new income, and your wage replacement checks will stop. Furthermore, if your new job requires physical labor that your doctor explicitly forbade, the insurer will use that as proof you were faking your injury, and they will terminate your medical benefits.

Do I have to mention my workers’ comp claim in future job interviews?

No. Under the Americans with Disabilities Act (ADA), a potential employer cannot legally ask you about past workers’ compensation claims or medical histories during a job interview. They can only ask if you are physically capable of performing the essential functions of the job with or without a reasonable accommodation.

Will the insurance company spy on me if I quit?

Yes. In 2026, digital and physical surveillance is standard protocol. If you quit your job but demand ongoing medical benefits, the insurance adjuster will heavily scrutinize your claim. They will hire private investigators to monitor your house and scrape your LinkedIn, Facebook, and Instagram to see if you are working a new job “under the table” or engaging in physical activities you claimed you could not do.